Market Watch Q1

Competition Heating up as the Market Enters Spring

Prices Rise to 8-Month High

The Greater Toronto Area housing market entered the spring season in an increasingly more competitive environment. The average selling price reached $1.109m in March, rising 1.1% month-over-month. Homes sold for an average of 100% of list price for the first time since June 2022, illustrating the more competitive market environment for buyers.

Compared to the market peak in March 2022, seen in the graph above, average prices were down 17.8%. This is the largest annual decline in average prices since the early 1990s. Compared to three years ago at the start of the pandemic, average prices were up 22.8%.

Detached homes recorded the largest annual decline in average prices at 19.9%, but also recorded the largest annual increase in average prices in the period to February 2022 at 31.2%. Compared to three years ago just prior to the pandemic, prices increased the most for detached homes with 29% growth, compared to 25% growth for semis/rows/towns and just 6% growth for condo apartment prices.

Quick Drop in Condo Supply during Q1

A notable bounce in sales occurred as the population surged and some pent-up demand was unleashed following a decline in fixed-term interest rates. Meanwhile, supply remained low as existing homeowners were hesitant to list with prices still well off their peak and move-up buyers continued to face affordability barriers.

Sales grew 45% month-over-month, exceeding the 10-year average February-to-March increase of 37%. Low listings were a key factor restraining sales activity. New listings dropped 44% annually in March.

Inventory dropped below 2.0 months of supply across the market in March. Condos have experienced a particularly notable decline in inventory over the past two months, falling from 3.9 months in January to 1.9 months in March. Detached inventory fell to a 12-month low of 1.5 months, while inventory for semis/rows/towns was lowest of any housing type at only 1.0 month of supply in March.

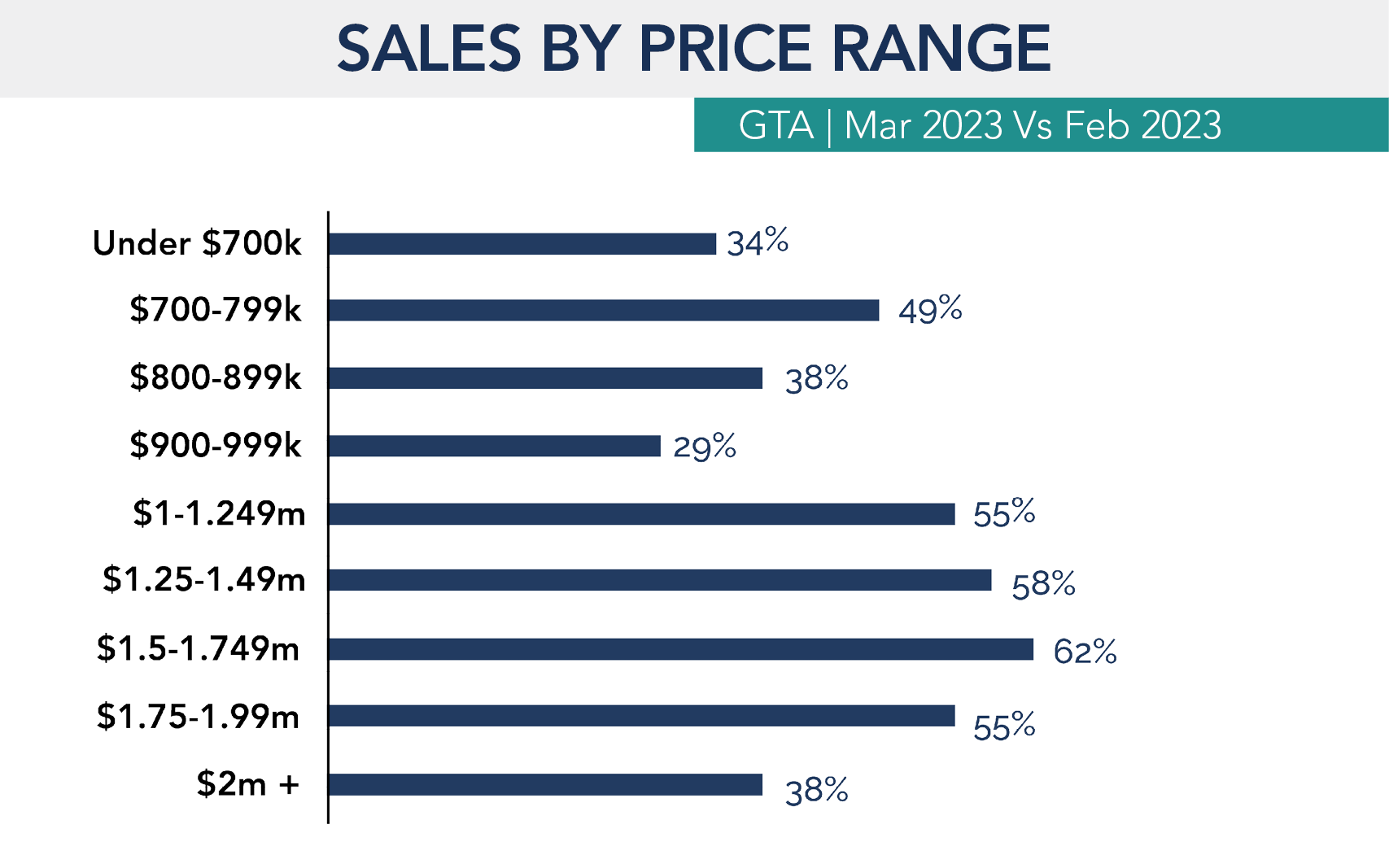

Monthly Sales Momentum Strongest for $1.0 to $1.9 Million Homes

On a monthly basis, sales momentum was strongest in the 1m-1.9m price range, with activity rising 57% from February. While posting strong month-over-month growth, momentum was relatively slower in the under $1.0 million and $2.0 million-plus segments, where activity rose 36% and 38%, respectively.

On an annual basis, sales in March were down the most for the highest priced properties. With activity falling 61% annually for homes in the $1.5 million price range. The only segment to experience annual growth in sales was homes under $700K, which saw a 30% rise in volume that was mostly owing to price depreciation pushing more homes under this threshold

Annual Price Declines Lowest in Central Toronto for All Property Types

Across all housing types, inventory levels were lowest in the 905 region of the GTA, falling to 1.3 months for detached homes, 0.9 months for semis/rows/towns, and 1.7 months for condo apartments.

Annual declines in median detached prices of 14% were equal in both the City of Toronto and 905 region, with the smallest decrease of 11% found in Central Toronto.

The smallest annual price declines for semis/rows/towns and condo apartments at 11% and 10%, respectively, were also identified in Central Toronto

Market Health based on Supply Levels

Seller’s Market = 4 months of inventory or less

Balanced Market = 4 - 6 months of inventory

Buyer’s Market = 6 months of inventory or more

As sales improved and active listings remained 32% below the 20-year average, months of supply dropped from 3.0 in January to 1.5 in March— the lowest inventory level since April 2022.

Supply will eventually rise as more mortgages begin to renew and people can no longer put off life-related decisions related to housing, but this should be offset by increasing levels of demand as buyers continue to become more comfortable with current interest rates and the population expands. However, affordability barriers should limit the ability for prices to rise meaningfully, holding the market in a state of balance.

What’s Next?

Bad news in the financial sector in the U.S. was good news for the GTA housing market, as the failure of Silicon Valley Bank and Signature Bank caused a 60-basis point drop in five-year Government of Canada bond yields during March, leading to some reduction in fixed-term mortgage rates.

The Bank of Canada is projecting a “soft landing” for the economy, with inflation (reported at 5.2% in February) returning to its 3% target by mid-year and 2% by the end of 2024. This should bring interest rates gradually lower while allowing for modest increases in unemployment, currently resting at near record lows.

Despite the increased presence of multiple offers, selling prices have faced modest upward pressure so far as higher interest rates have restrained buying power. However, with the population increasing at a record pace, and homebuilding activity slowing, the housing supply deficit will continue to grow and add further fuel to housing prices over the medium and longer term.

In the short-term, prices are expected to continue gradually recovering. More supply will eventually arrive on the market at some point this year as listings return towards a more normal level, partly due to existing homeowners taking advantage of improved selling prices and partly due to financial difficulties being experienced due to the sharp rise in the cost of debt. At the same time, demand should continue to rebound off its 2022 lows but remain well below peak levels in 2021, supporting balanced conditions.