Market Watch Q2

Let’s Review this past quarter!

Sales continue to moderate from record highs but remain elevated

Sales slowed the most for condo apartments between April and May, recording an 18% month over month decrease compared to declines of semi/row/town houses. As a result, supply levels for condo apartments grew to 1.4 months the highest level of the year.

If we take a look at Q2 of 2020 and 2021. We did 16,282 sales in Q2 of last year, this year we had 36,720. Up by 125%!!

So again, you saw that March was the busiest month in terms of sales. And then all of a sudden, April, May and June had dropped a little bit. This gives the illusion that the market is really starting to slow down. However, compared to last year, we're up 125%. Amazing!!

Some Heat Comes off the Condominium Market as Average Prices Near $700K

While market conditions remained tight for condo apartments, average prices dipped by 1.4% in May after reaching a record high in April.

Meanwhile, average prices for detached houses continued to trend higher, posting a 2.0% month-over-month gain to reach above $1.4 million for the first time, with prices 37.0% higher than a year ago.

Within the semi/row/town category, price increases were relatively more modest at 0.7% month-over-month and 24.6%-year over- year.

What about prices in Q2?

872k was your average price in the second quarter of last year. 1.1 million this year, that's up by 26%.

So the first half of the year did 44,000 sales in the first half of 2019. This year we are at 70,270, up by 94%. There have been years were 70k sales were the number for the complete year! That’s insane!

Change in Detached sales in the past 3 months

In comparing sales in May to three months earlier in February, activity was up 9% across the GTA.

Within the detached category, sales were up 16%, driven by growth in the low-end of the market under $600K and between $700 and 899K, and also the high-end of the market above $1.75 million.

In fact, the fastest growing sales segment over the past three months was detached homes over $2.0 million, which increased 31%.

For condo apartments, sales in May were down 13% compared to three months earlier, dragged down by activity under $700K.

All sales segment for condo apartments above $700K were up in the past three months, led by a 33% surge in sales above $1 million

What is a Supply Indicator?

The volume of new listings arriving on the market also slowed over the past two months, but by a lesser degree than sales, resulting in a slightly more balanced market compared to recent months but still considered tight and characteristic of a seller’s market.

While active listings reached their highest May level in five years, supply was equal to only 1.0 month of inventory, up from the March low of 0.7 but less than half the 10-year average of 2.1 months.

Furthermore, the ratio of sales-to-new-listings at 64% stayed above the upper boundary a balanced market (60%), with homes selling at an average of only 11 days (10-year average of 23 days) and for an average of 105.6% of listing prices (10-year average of 99.9%).

What’s a Price Indicator?

The continued strength in the market led to further upward pressure on prices in May.

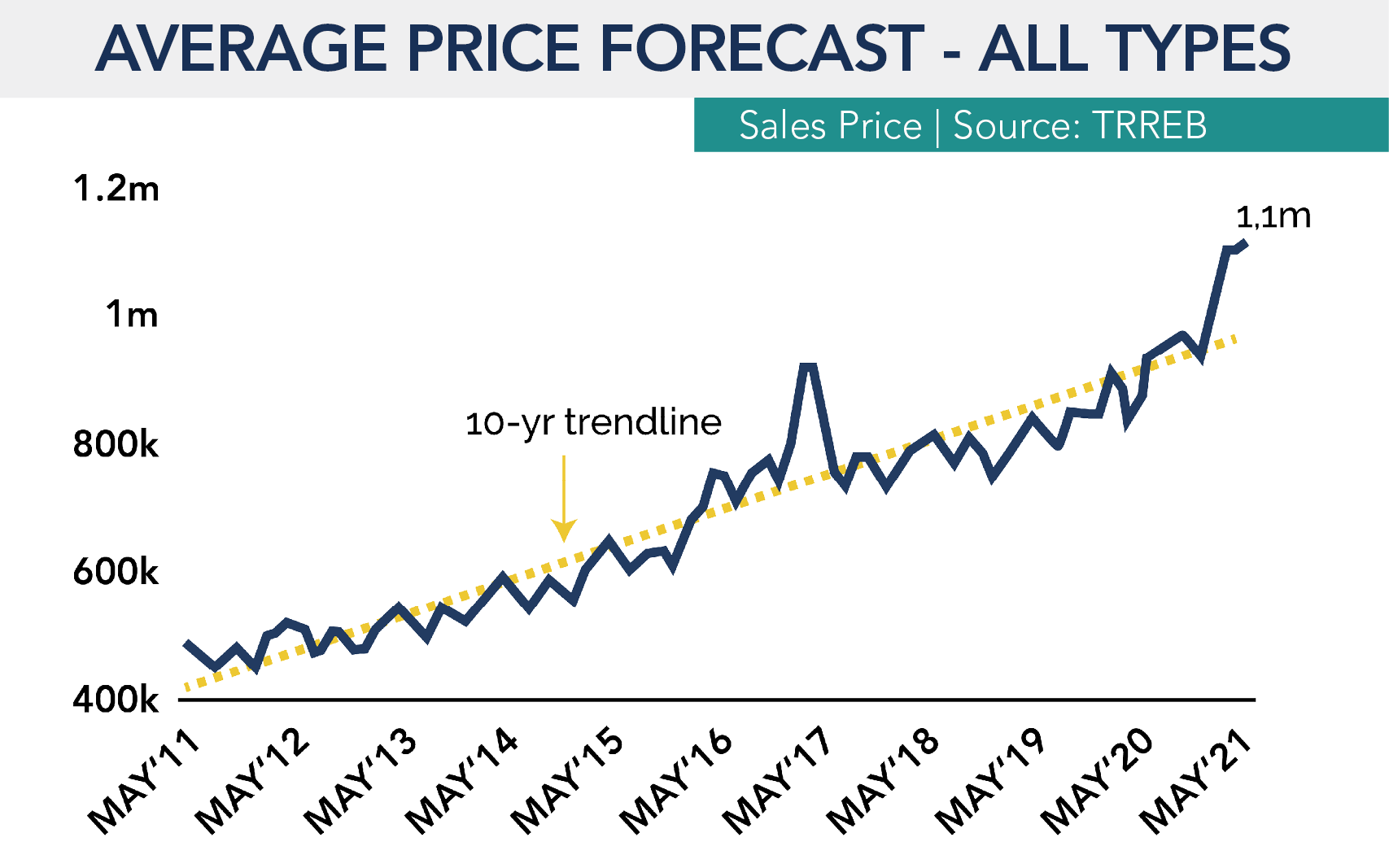

The average selling price reached above $1.1 million for the first time ever, increasing 1.6% from April and 28.4% from a year ago.

On a month-to-month basis, price increases have been generally slowing over past couple months, but continue to remain supported by high demand and low supply.

With the current average price about 13% higher than the 10-year trend level, it is likely that prices will continue levelling out in the coming months as buyers act less aggressively following the strong run-up over the past year.

So What’s to come next?

You're probably feeling that it’s starting to slow a little bit in July. And I agree. So the question is why?

well, we got buyer fatigue, we got seller fatigue, and we got agent fatigue. I mean, everybody's just tired.

Since COVID restrictions being lifted. We have semi warm weather. I think people just needed to rest and say “I just got to slow down” . It's been so crazy. So it's probably gonna slow down a little bit in July and August, but it'll still be a very, very strong market .

I think what we're gonna see in the fall, once the kids go back to school, Labor Day's over with, I think we're gonna have a very decent market again. And it will continue. And I think we're gonna close out a very strong year. At least that's my opinion.

If you want a specific update on your neighborhood’s market don’t hesitate to reach out, let me buy you a coffee!